Racial Differences in the Demand for Cash Value Life Insurance

Abstract

Within the past decade, there has been widespread encouragement for consumers to hedge their wealth by investing in financial products such as cash value life insurance (CVLI). Though most individuals invest in life insurance to cover expenses after a loved one has passed, many financial advisors are trying to enlighten consumers on other beneficial uses of insurance. This study explores racial differences in the demand for cash value life insurance. Using data from the 2010-2019 Survey of Consumer Finances, I identify factors that impact the trend in demand toward CVLI. While previous literature focused on the ability to purchase life insurance and how much to insure, this work examines differences in preference by race. The findings suggest that Black Americans have decreased their demand for cash value life insurance, while White Americans have increased their demand for life insurance over the past decade.

Introduction

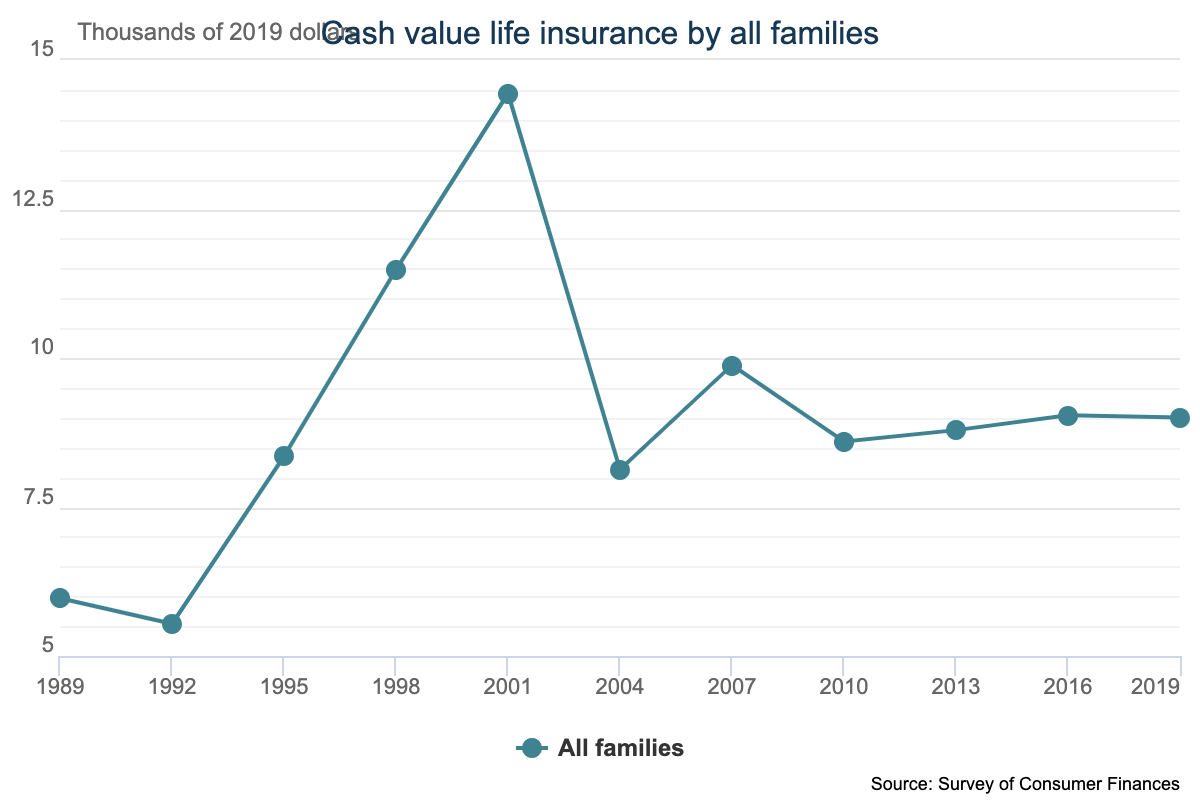

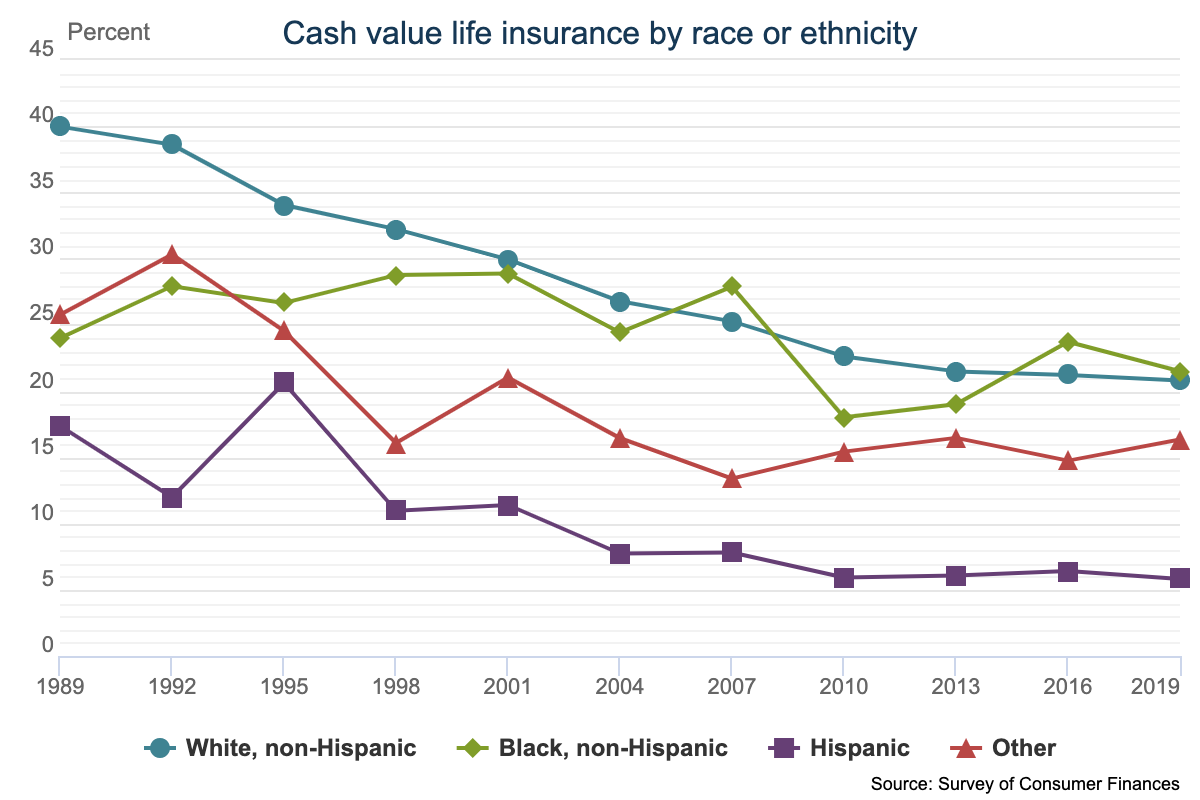

Within the past decade, the percentage of all households investing in cash value life insurance (CVLI) has decreased. Figure 1 shows a sharp decline after 2001 and then the trend flattens from 2010 until present. The trend appears to be much more volatile when examined by race, as shown in Figure 2. While Mulholland et al. (2015) conclude demographic breakdown is not a sufficient indicator for change in demand, data from the Survey of Consumer Finance (SCF) may lead to a different finding. Part of the reason for racial differences in the demand for life insurance may be economic inequality, as research has shown that White families have higher net worth than Black American families. Notably, the high differences in net worth imply a significant racial wealth gap. Surveys conducted to determine the views of both White and Black-Americans regarding life insurance have established that Black-Americans tend to perceive life insurance a way of passing their wealth inter-generationally.

Figure 1

Figure 2

The SCF established that the number of Black Americans with life insurance is lower than that of White individuals. Similarly, Black Americans acknowledge that in the event of their death, their families are likely to face challenges in their financial future (Medine, 2020). Racial differences in the demand for life insurance can be dated back to the late 19th century when high levels of racial disparity occurred in part because insurance companies were openly biased against Black Americans. During this period Black Americans who obtained life insurance were given fewer benefits at a higher cost than other races (Medine, 2020). This open racial bias by the insurance companies only gradually came to a halt with the rise of the Civil Rights Movement. Finally, Black Americans are reluctant to purchase life insurance, believing it to be unaffordable while other races view the cost as affordable. Not only have Black Americans felt this financial product is out of reach for their financial situation, but significant mistrust has also been established with these financial institutions due to fear of being taken advantage of. Historical mistrust can be dated back to the 1860s when the Freedman’s Savings and Trust Company failed, causing thousands of Black Americans to experience devastating financial losses (Booth, 2020). As a result, Black Americans have become more risk averse when it comes to their finances since they cannot afford to take any financial losses.

This paper tests the hypothesis that the demand for cash value life insurance varies by race. While much research has focused on the factors that impact overall demand for life insurance (Gutter, Hatcher, 2008), shifts in demand for cash value life insurance (Mulholland et al., 2016), and the attractiveness of life insurance, little research has been done to show the demographic breakdown of the demand for these products. By studying the racial differences in demand for cash life insurance, we may find that a “one size fits all” approach to consumer behavior is mistaken. A regression analysis will study whether there is a “race effect” on insurance demand apart from other explanatory variables.

Background

There have been significant shifts in the demand for cash value life insurance in recent years driven by different demand forces. Demand increases are mainly related to changes in the traditional uses for this type of insurance. CVLI can now be used to save for retirement The money placed in the policy grows tax-deferred, and can be accessed tax-free in retirement. CVLI can now be used as well to help pay for long-term care expenses, a growing concern as long-term care costs continue to rise. It can provide a way to pay for these expenses without depleting other savings or retirement accounts. The death benefit from a CVLI policy can now be used to help pay for estate taxes. (Mulholland et al., 2016). Since the traditional uses for CVLI have expanded, more people are now using it as an investment tool. While many people use the coverage to “pay off debt [or] generate liquidity for estates,” (Parrish, 2020) businesses use it specifically for investment purposes. The Pension Protection Act of 2006 improved retirement plans so that now CVLI can be used to address many financial needs beyond the passing of a loved one. Not only does it allow for “income” through various monetary payouts, but it allows the death benefit to be a part of the “investment” (Parrish, 2020).

Demand decreases have been due mainly to the Great Recession (2007-2009), the continuing rise in health care costs and increased popularity of alternatives to traditional life insurance products (Rabbani, 2020). The economic downturn negatively impacted the demand for CVLI because many people lost jobs or faced reduced hours, and could no longer afford to pay for their life insurance (Rabbani, 2020). The value of life insurance policies also decreased as the stock market declined. As a result, people were less likely to purchase or renew their existing policies.

The attractiveness of CVLI increases when families and consumers are faced with sudden hardship. The COVID-19 pandemic swept through the world, leaving many to deal with the costs of health and funeral expenses. Since many individuals did not foresee this rapid change in events, they were forced to scramble for money to cover the remaining expenses. Policyholders on the other hand were able to borrow against their coverage plans without terminating the plan. An added benefit was that the loan does not appear on the borrower’s credit report (Russell et al., 2018).

Data and Methodology

Data comes from the Survey of Consumer Finances (SCF) provided by the Federal Reserve Board. The SCF provides information on a triennial cross-sectional survey of U.S. families, and it covers a range of data topics including educational attainment, occupation, and housing characteristics on approximately 115,500 families each year. In this project, a sample of 267,765 individuals was used, including demographics and assets data from 2010, 2013, 2016, and 2019. The goal was to test whether Blacks have lower demand for CVLI.

The following logistic regression model is specified:

𝐶𝑎𝑠ℎ𝐿𝑖 = β0 + β1−4(𝑦𝑒𝑎𝑟) + β5−9(𝑎𝑔𝑒)+ β10−14(𝑖𝑛𝑐𝑜𝑚𝑒) + β15−18(𝑒𝑑𝑢𝑐𝑎𝑡𝑖𝑜𝑛) + β19(𝑟𝑖𝑠𝑘 aversion)+ β20(𝑚𝑎𝑟𝑟𝑖𝑎𝑔𝑒) + β21(𝑐ℎ𝑖𝑙𝑑𝑟𝑒𝑛) + β25(race) + ε

Where:

CashLi = Total CVLI held by household

Year = Survey year (2010, 2013, 2016, 2019)

Age group = Age group of respondent

Income group = Income quartile of respondent

Education = Education level of respondent

Risk = Respondent willing to take financial risk (yes=1, no=0)

Marriage = Marital status (married=1, single=0)

Children= Children in respondent’s household (1=one or more, 0=none)

RaceCl = Race of respondent (Black=1, Non-Black=0)

ε = Error term

Limitations and Details of the Model

The dependent variable (CVLI) does not consider a lapse in coverage over the given time period. The lapse in coverage could in theory introduce bias into the model, but given the small number of households with such lapses, no significant bias is likely. There is also no straightforward way to disaggregate the savings component associated with the insurance policy. Market responses to the COVID-19 pandemic are outside range of dates of the data.

Age is categorized as follows: less than 35 (=1), 35-44 (=2), 45-54 (=3), and 55-50 (=4). Income (measured as the total amount of annual income received by households in 2019 dollars) falls into four quartiles 0-24.9% (=1), 25-49.9% (=2), 50-74.9% (=3), and 75-100% (=4). Education is categorized based on the highest educational attainment during the time of the study (i.e., no high school diploma, high school diploma, some college, college degree and above). Racial group is defined as Black and non-Black.

Regression Results

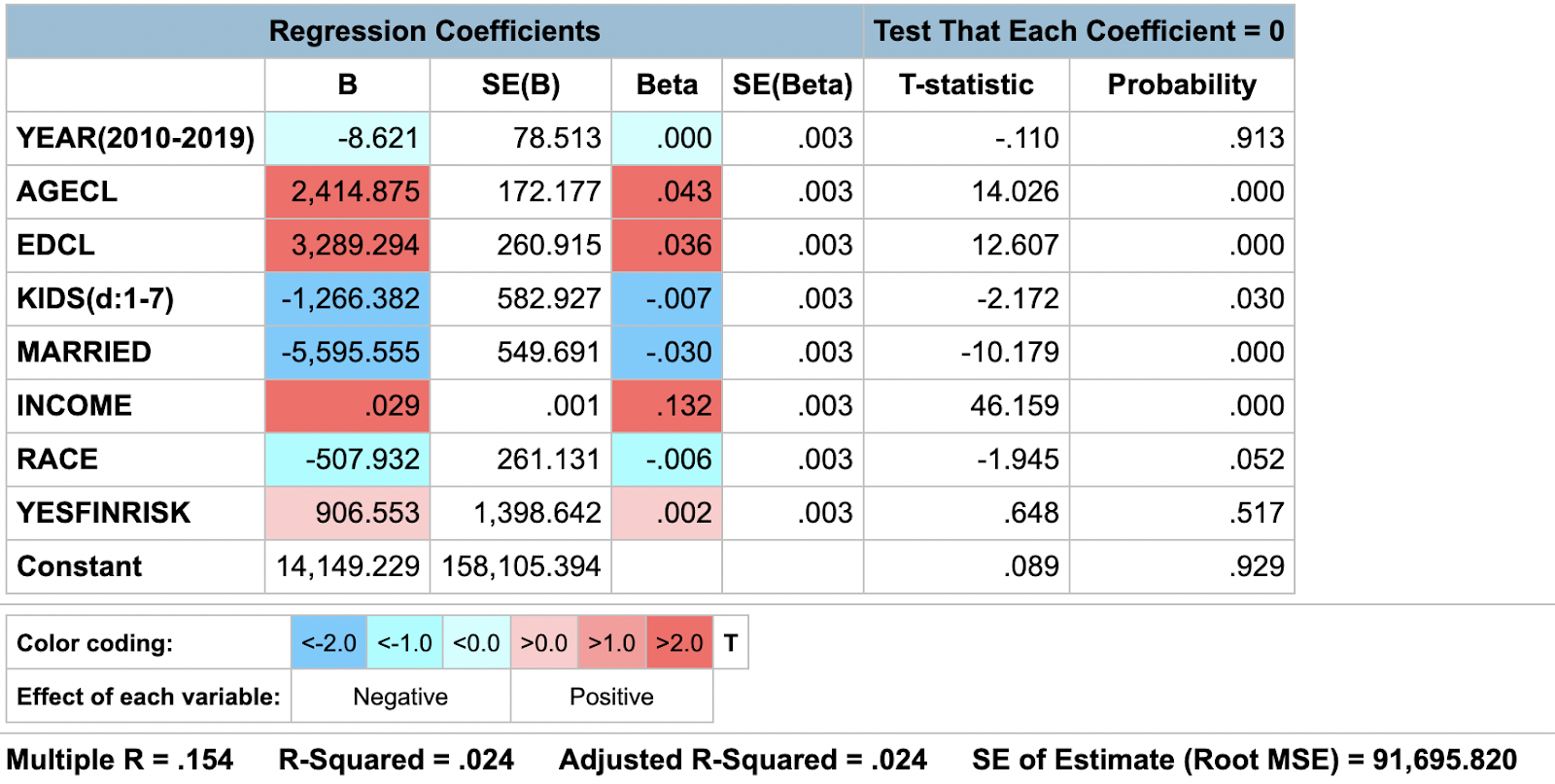

The empirical results are reported in the table below. The key independent variable – race –is associated with decreased holdings of CVLI by about $508. The control variables indicate that CVLI cash value life insurance holdings fell slightly over time. However, as individuals age, they increase their investments in CVLI. On the other hand, having one or more children reduces the CVLI held by individuals as does marriage. Risk taking is associated with greater CVLI holdings.

The overall explanatory level (R2) of CVLI at 2.4% suggests that there are other unmodeled factors affecting CVLI levels. Still the significance of the race variables at the 10% level (t = -0.945, p = -.052) indicates that being Black is associated with lower investment in CVLI.

Conclusion

This hypothesis test shows that there are significant disparities in CVLI. Discrimination and mistrust in financial advisors seem to have played a role in influencing the overall demand for financial products. We initially observed a large decrease in CVLI consumption after 2001 and a much more stable overall level in CVLI after 2010. However, when we examine the changes in CVLI associated with race over time, we found a significant disparity suffered by Black individuals.

References

Agesa, J., Agesa, R., & Berry, W. (2011). A History of Racial Exploitation in Life Insurance. Franklin Business & Law Journal, (3).

Gutter, M. S., & Hatcher, C. B. (2008). Racial differences in the demand for life insurance. Journal of Risk and Insurance, 75(3), 677-689.

Medine, T. (2020). Is there a life insurance race gap? Retrieved from Haven Life: http://www.havellife.com Mulholland, B., Finke, M., & Huston, S. (2016). Understanding the shift in demand for cash value life insurance. Risk Management and Insurance Review,19(1), 7-36.

Parrish, S. (2020). Recognizing Cash Value Life Insurance as an Investment.

Rabbani, A. G. (2020). Cash value life insurance ownership among young adults: The role of self-discipline and risk tolerance. Journal of Behavioral and Experimental Finance, 27, 100385.

Russell, D., Chong, J., & Phillips, M. (2018, March 27). Raising Cash Under Duress And The Role of Cash Value Life Insurance: An Educational Example.

Walden, M. L. (1985). The whole life insurance policy as an options package: an empirical investigation. Journal of Risk and Insurance, 44-58.